A variational formula for risk-sensitive control

Presenter

May 9, 2018

Keywords:

- risk-sensitive control; variational formula; principle eigenvalue; Collatz-Wielandt formula

MSC:

- 94E20

Abstract

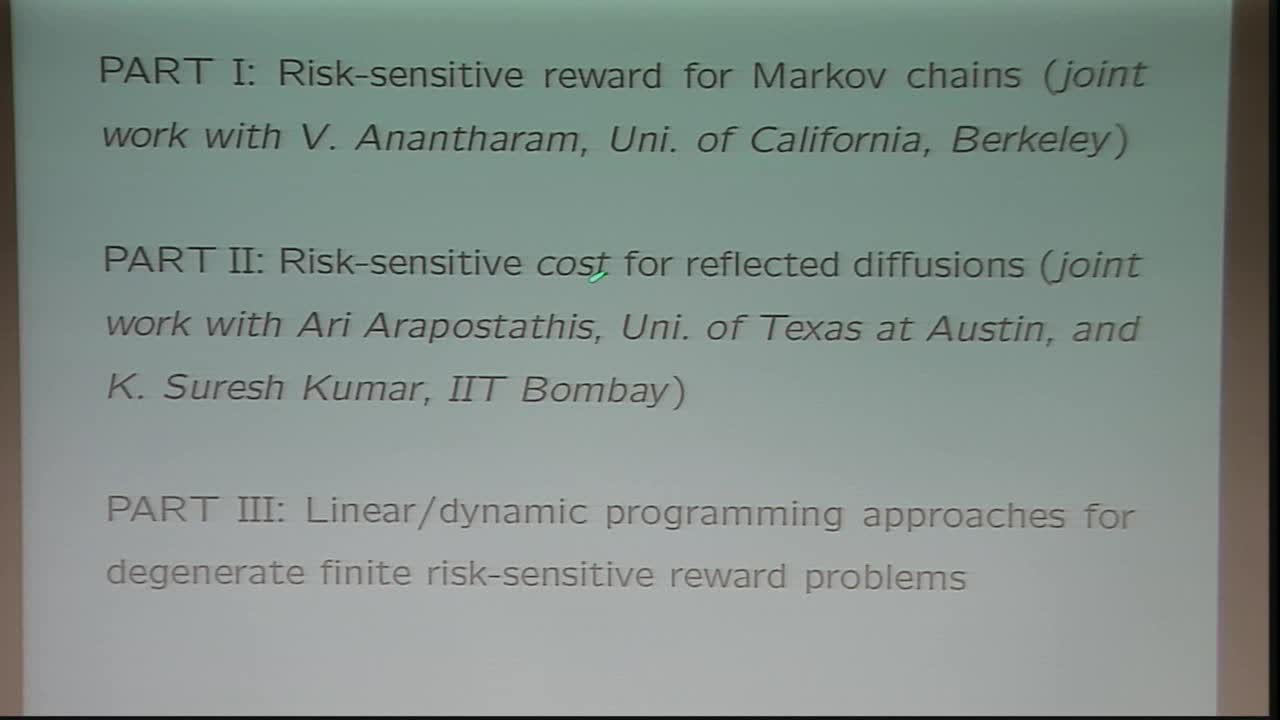

This talk will describe a variational formula for risk-sensitive reward. This extends the Donsker-Varadhan characterization of principal eigenvalue of a non-negative matrix in discrete case and an elliptic operator in the continuous case. One application to linear and dynamic programming approaches for risk-sensitive control of finite Markov chains without the irreducibility assumption will be described. This is joint work with V. Anantharam (UC Berkeley), A. Arapostathis (UT Austin) and K. Suresh Kumar (IIT Bombay).